Master Algorithmic Trading: A Beginner’s Guide to Backtesting

Quantconnect is an online platform that allows developers and traders to design, backtest and execute algorithmic trading strategies across different financial markets. I have been using Quantconnect for 3 years, have run over 1700+ backtests, and now live trade on the platform. In this tutorial, I will provide a step-by-step guide to help you get started with Quantconnect.

Table of Contents

- Creating a Quantconnect account

- Ramping up with the Learning Center

- Backtesting your algorithm

- Deploying your algorithm to paper trading

- Avoid making the same mistakes as me

- Final words

Creating a Quantconnect account

To get started with Quantconnect, the first step is to create an account. Go to the Quantconnect website and click on the “Sign up” button. Fill in your details and agree to the terms and conditions. Once you have verified your email address, you can log in to your Quantconnect account. The online platform features a fully functional IDE in either Python or C#.

At the time of writing, the free tier allows you to run either one backtest or one research node at a time for free. A research node is a jupyter notebook environment useful for analyzing all the data. I recommend you make use of this as much as possible before signing up. The main datasets are available to you except for some notable sets such as the tick data. Personally, I have spent nearly two years exploring algorithms and data on Quantconnect before actually signing up for live trading.

Ramping up with the Learning Center

Before trusting a platform with your money, make sure to understand it well. In order, I recommend that you start by reading through the documentation, follow a few courses in the learning center, and then browse the forums for ideas and support. You will need to master the key concepts such as the handling of time. You will also have the opportunity to try out the algorithm framework. It is a powerful tool that provides structure to your algorithms.

Backtesting your algorithm

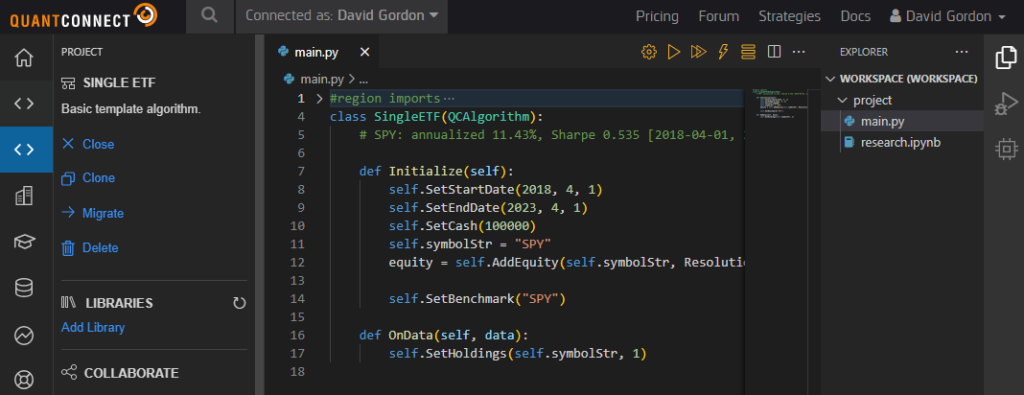

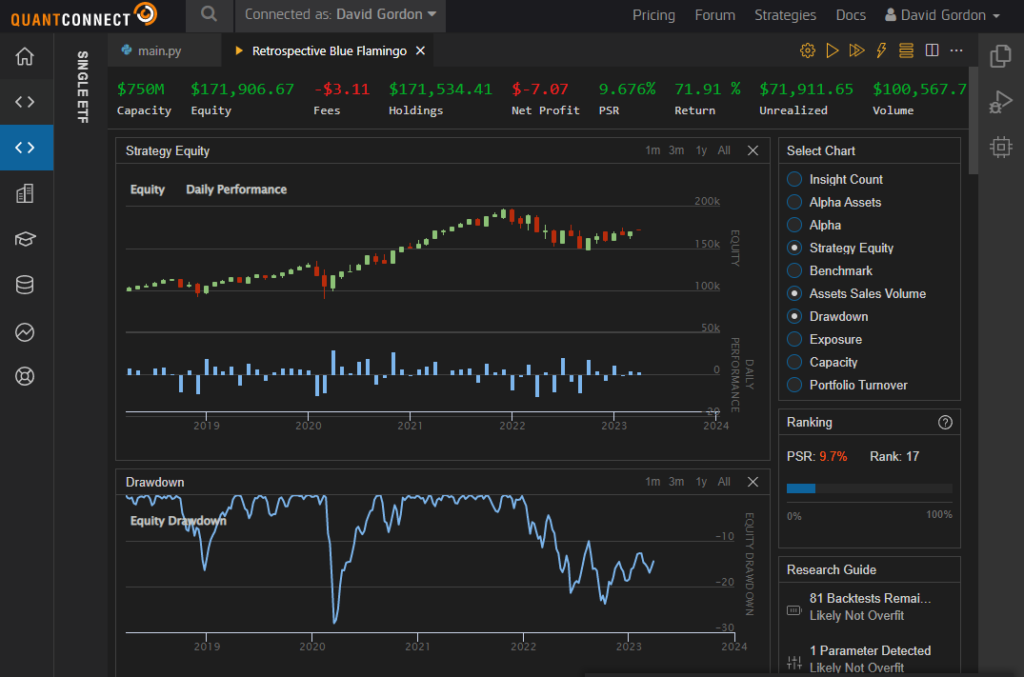

By now, you have setup a few projects as you followed the courses. Now, it’s time to start your own project. Once you have set up your project, you can start coding your algorithm. Quantconnect provides a code editor where you can write your code, and the platform supports several libraries that you can use for financial analysis and trading. Once you have written your code, you can backtest your algorithm by clicking on the “Backtest” button. Quantconnect will simulate how your algorithm would have performed in the past based on historical data.

Deploying your algorithm to live trading

Before moving to live trading, I strongly suggest spending time paper trading with Quantconnect first and then with your personal broker. The live algorithm that I am live trading now spent 8 months in paper trading before I worked out all the kinks and built enough trust to manage part of my portfolio. My experience and timeline will not be the same as yours and hopefully my posts will help you accelerate your journey.

If you are satisfied with the backtest and paper trading results, you can deploy your algorithm to live trading. However, before you can do that, you need to connect your trading account to Quantconnect. Quantconnect supports several brokers, and you can choose the one you want to use. I will be covering the details of live trading in its own post.

Avoid making the same mistakes as me

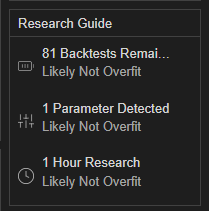

The first mistake I made is overfitting. This happens when the algorithm performs well with in sample data (or historically) and terrible when data is out of sample (or live). Many algorithms in the forums will show excellent backtests. It’s very tempting to use them as is, but keep in mind that many of them suffer from overfitting. I fell into another trap of overfitting when I fell in love with a particular algorithm. I spent hours and hours tweaking parameters only to find that I had overfit. Pay attention to the metrics (# of backtests, # of parameters, # hours research) in the bottom right of your backtest screen. They are a good indication that you’ve spent too much time on your algorithm.

The second mistake I made is complexifying. A complex algorithm is not always better. The most powerful idea is a simple one. Complexity gets in the way of troubleshooting and optimizing. When the algorithm starts drifting away from the original premise, I would argue that I am eventually losing alpha. Typically, I will keep adding parameters and conditions in an effort to improve performance incrementally. Over time, the complexity exceeds the benefits.

Final words

Quantconnect is an excellent platform for developing and testing algorithmic trading strategies. In this tutorial, we have provided a step-by-step guide to help you get started with Quantconnect. By following these instructions, you should be able to set up a new project, code your algorithm, backtest it, and deploy it to paper trading. However, remember that algorithmic trading is a complex process that requires careful planning and testing. Always be prepared to make changes to your strategy if necessary. Stay tuned for more posts and enjoy backtesting your new ideas!